How to Finance an ADU in San Diego

8 min read

You have two primary paths: keep your current mortgage and borrow against home equity via a HELOC/home-equity loan, or refinance into a construction/renovation (or cash-out) mortgage that can underwrite your after-improvement value and fund the build in draws (NerdWallet). Equity options help you preserve a low first-lien rate, while construction/renovation loans are useful when equity is tight. San Diego homeowners may also pair financing with the SDHC ADU Finance Program, which offers low-interest construction-to-permanent loans plus free technical assistance for eligible owner-occupants (San Diego Housing Commission, NerdWallet).

Quick takeaways

- Best-fit Accessory Dwelling Unit (ADU) loan options: keep your low-rate first on your primary residence and borrow equity (HELOC/home-equity) or refi into construction/renovation financing so underwriting uses your after-improvement appraised value. (NerdWallet)

- SDHC ADU Finance Program (City of SD): up to $250,000, 1% during construction, then 4% fixed/15-yr permanent loan; 7-year affordability covenant—helpful when interest rate market conditions are high. (San Diego Housing Commission)

- CalHFA $40k ADU Grant Program: fully allocated as of Dec 28, 2023—monitor for future rounds as part of your ADU financing plan. (CalHFA)

- Fees: Impact fees waived under 750 sq ft statewide; school fees may apply >500 sq ft (district-set)—confirm alongside building permits. (HCD ADU Handbook 2025)

- Costs: Typical San Diego construction costs $375–$600+/sq ft depending on scope/site (mid-level projects often $375–$450/sq ft). (Platform/Ikkonic – San Diego)

San Diego–Specific Programs & Grants

SDHC ADU Finance Program (City of San Diego)

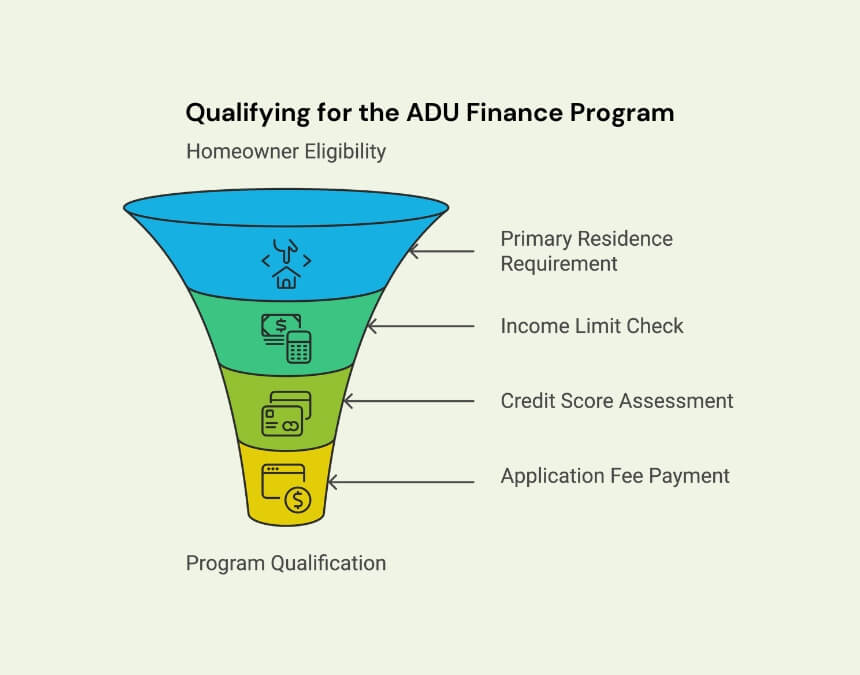

What it is: Construction-to-permanent construction financing plus free technical assistance for moderate-income, owner-occupant homeowners in the City of San Diego—ideal when adding an in-law suite/guest house for multi-generational living. (SDHC)

Key terms: Up to $250,000; 1% fixed during construction; converts to a 4% fixed, 15-year permanent loan (due in 30); up to 75% LTV; 7-year affordability covenant (≤80% AMI rents; no renting to family during the covenant). (SDHC)

Eligibility: Income up to $236,600 (150% AMI); owner-occupied detached SFR within city limits; 680+ Credit Score (FICO); $2,500 application fee at construction-loan closing. (SDHC)

Tip: If you qualify, SDHC’s below-market loan products can reduce carrying costs; some owners pair SDHC with a small Home Equity line of credit (HELOC) for overages.

CalHFA $40,000 ADU Grant (statewide)

Status: Fully allocated as of December 28, 2023 under the CalHFA ADU Grant Program; it previously reimbursed up to $40,000 for pre-development and certain closing costs. Monitor CalHFA bulletins for any future appropriations. (CalHFA)

ADU Bonus (Density) Program – City of San Diego

What it is: A local density bonus allowing additional ADUs when units are deed-restricted affordable for 15 years; rules vary inside Transit Priority Areas (TPAs) versus outside and must align with zoning regulations and local municipalities’ review. (City of San Diego)

2025 update: The Mayor’s office advanced reforms on scale/compatibility, parking outside TPAs, fire safety, penalties for covenant violations, and AB 1033 condo-sale implementation; final provisions await City Council action. (City memo)

Pre-qualify before design fees: confirm owner-occupancy, 150% AMI and ~680+ FICO, then lock the 1% construction phase—pair with a small HELOC to cover overages.

Core Financing Options

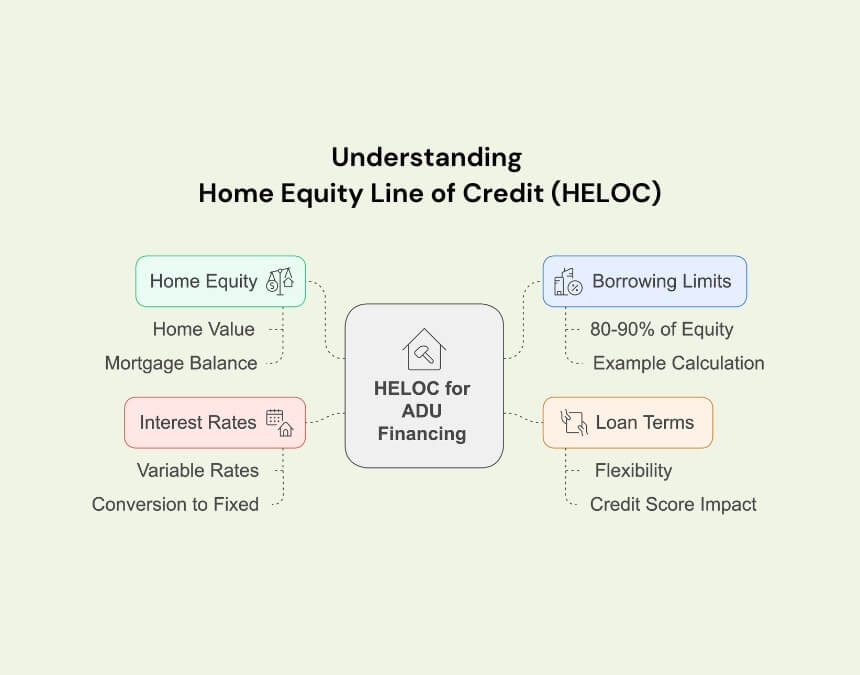

HELOC (Home Equity Line of Credit)

What it is: A HELOC is a revolving Home Equity line of credit secured by your main house—use it as needed during the design process and pay interest only on the amount you draw; you keep your existing first mortgage intact (often an adjustable rate per lender policies). (CFPB overview)

Best for: Preserving a low-rate first mortgage while flexibly funding an ADU, accessory apartment, or back yard cottage. (NerdWallet on ADU financing paths)

Watch-outs: Typically variable rates; verify margin, caps, and repayment features (including any interest-only loan period) with your lender. (CFPB)

Preserve a great first-lien rate with a HELOC; stage draws with your build schedule and ask about fixed-rate conversion options to cap exposure if rates rise.

Home-Equity Loan (Fixed-Rate Second)

What it is: A home-equity loan is a lump-sum, fixed-rate second with predictable payments; it doesn’t replace your first mortgage. (Investopedia explainer)

Best for: Homeowners who want payment certainty and to keep their current first lien while adding an ADU for multi-generational living or a home office.

Watch-outs: Size is limited by appraisal and lender CLTV rules; rates are often higher than first-lien mortgages. (Investopedia)

Great for predictable cash flow—keeps your low first intact. Sizing is CLTV-limited, so verify appraisal early and match payment to your ADU construction timeline.

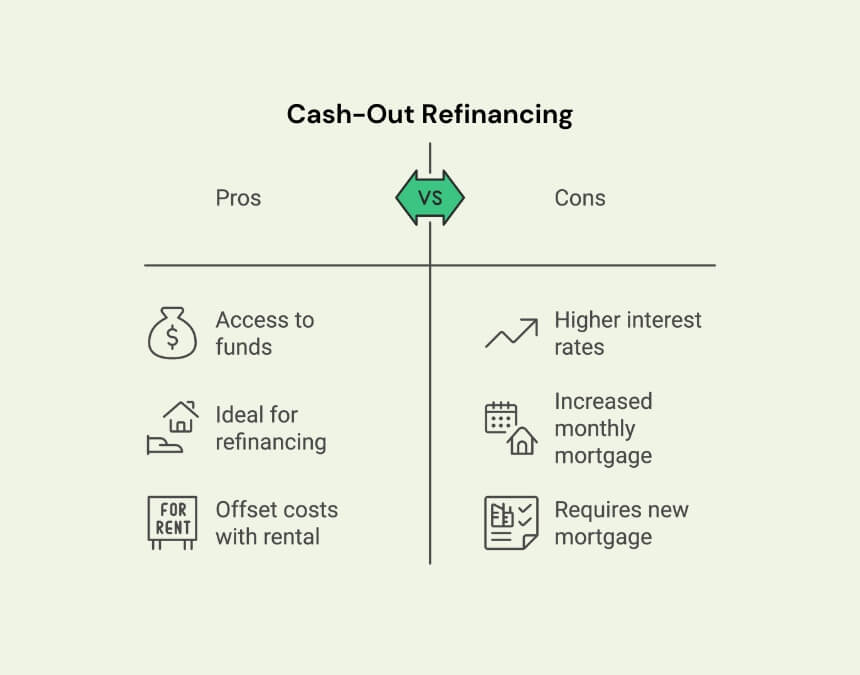

Cash-Out Refinance

What it is: A cash-out refi replaces your existing mortgage with a larger first-lien and gives you the difference in cash for the ADU—one loan/one payment under current market conditions. (NerdWallet ADU financing guide)

Best for: Owners already planning to refinance loans or needing a large lump sum for utility connections and finishes.

Watch-outs: Potentially higher rate than your current loan; factor in closing costs and break-even math. (NerdWallet)

Run a break-even: higher rate and closing costs must be offset by ADU rent. If your first-lien rate is low, compare equity seconds before refinancing.

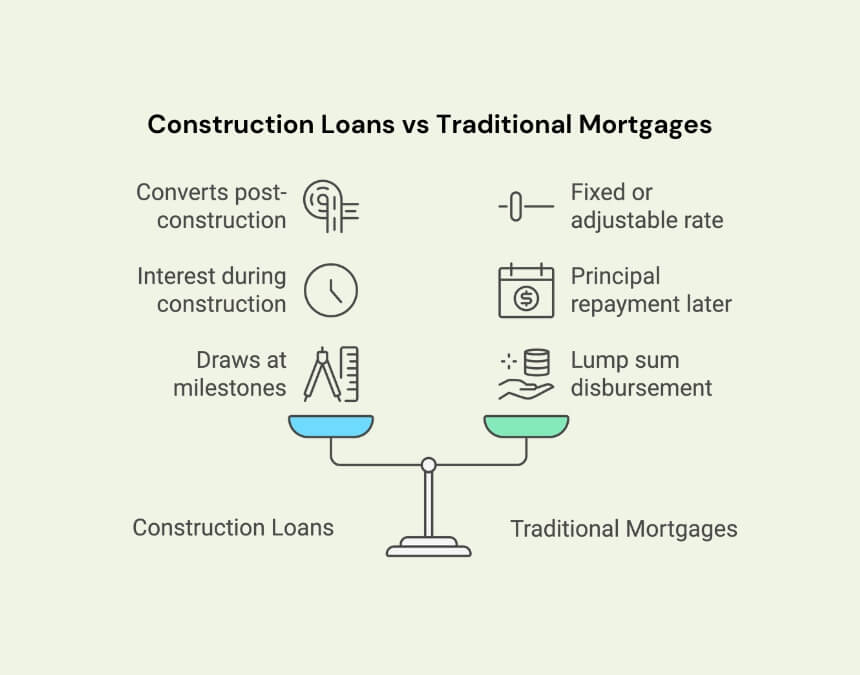

Construction Loan (Construction-to-Permanent)

What it is: A construction-to-permanent loan funds your build in milestone draws and underwrites on the home’s after-improvement value; after completion, it converts to a permanent mortgage (often replacing your first). (NerdWallet)

Best for: Low-equity owners or larger scopes that exceed equity limits, including Conversion ADUs and detached living quarters.

Watch-outs: More documentation, inspections, and closing steps; plan draw schedules, contingency, and coordination with your building team/project manager.

Low equity? Use construction-to-perm under after-improvement value. Have stamped plans, budget, and a GC contract ready to speed underwriting and draw approvals.

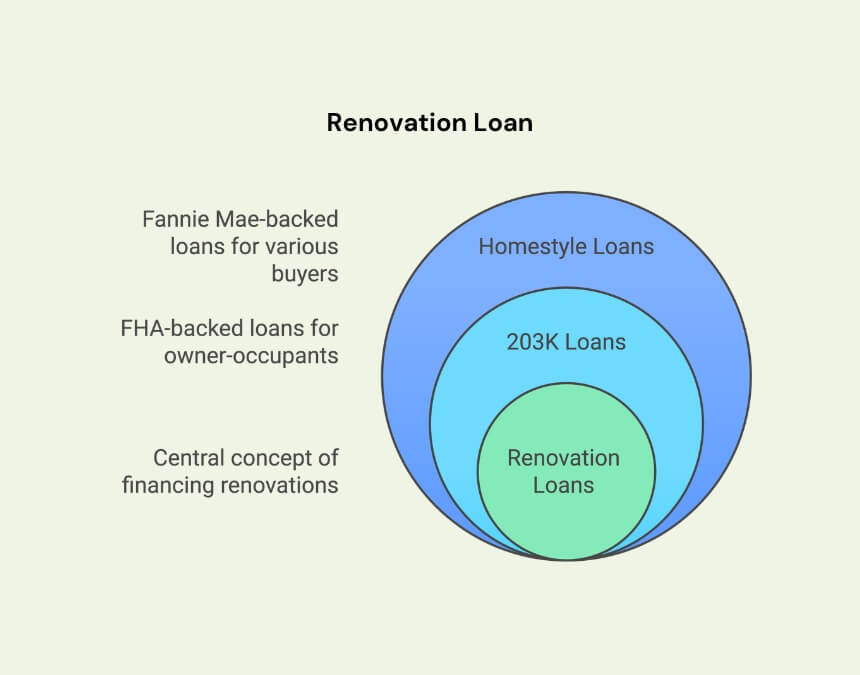

Renovation Loans (FHA 203(k) / Fannie Mae HomeStyle®)

What it is: Renovation mortgages bundle a purchase or refi with renovation funds and qualify on future value; common programs are FHA 203(k) and Fannie Mae HomeStyle® Renovation. (NerdWallet, HUD 203(k) overview, Fannie Mae HomeStyle)

Best for: Buying a single-family home with plans to add an ADU or adding an ADU when equity is limited.

Watch-outs: Program rules (approved contractors, MI/fees), paperwork, and timeline management through city plan check and inspections.

Ideal for purchase-plus-ADU or limited equity: qualifies on future value. Expect stricter contractor oversight, contingency reserves, and inspection-based disbursements.

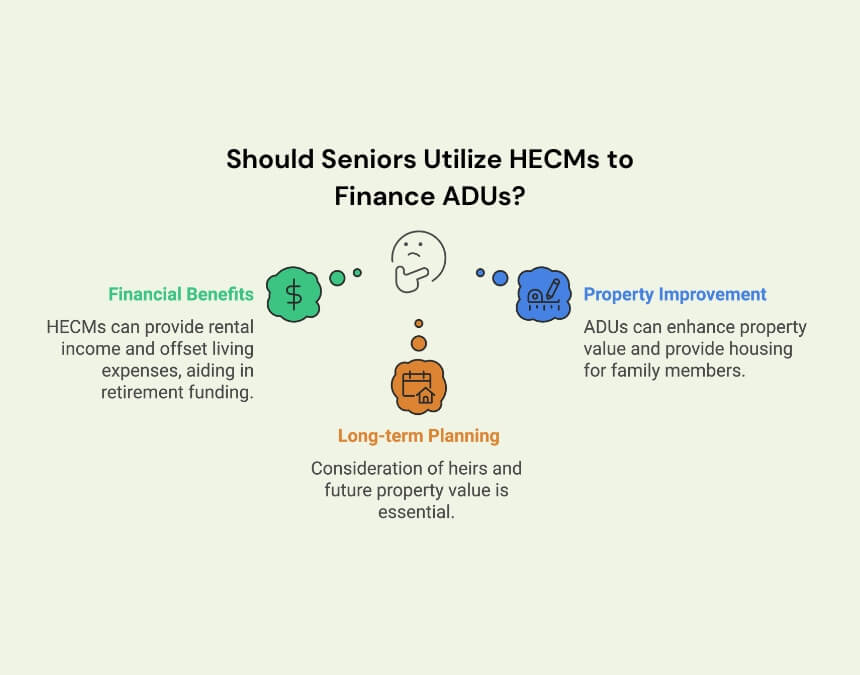

HECM (Reverse Mortgage, 62+)

What it is: A HECM lets homeowners 62+ tap equity with no monthly mortgage payment; the loan becomes due when the home is sold, the borrower moves out, or passes away. (HUD HECM basics)

Best for: Seniors funding an ADU for caregiving, downsizing on-site, or creating an income-producing rental next to the main house.

Watch-outs: Interest/fees accrue and reduce remaining equity; independent counseling is required before proceeding. (HUD)

A HECM can fund an ADU with no monthly mortgage payment—plan for accruing interest, loop in heirs, and prioritize designs that generate stable rental income.

Costs, Fees & What To Budget (San Diego)

- Build cost planning: For budgeting, plan on $375–$600+ per sq ft for a turnkey detached ADU; scope, site work, utility connections (e.g., sewer line/electrical), and finishes drive the range—plus market factors like supply chains and energy-efficient upgrades (e.g., solar PV). See the San Diego market snapshot here. (Platform guide)

- Impact fees: Waived for ADUs under 750 sq ft statewide; for larger ADUs, fees must be proportional to the primary home and are assessed during permitting under local building codes. (CalHCD ADU Handbook, 2025)

- School fees: School districts may levy fees when an ADU is over 500 sq ft; confirm your district’s current schedule prior to City plan check or permit issuance. (CalHCD ADU Handbook, 2025)

Caution: “A lot of times people… think their ADU will cost $100k and it’s $300k. That’s going to stop the loan process in its tracks.” — James Carmody, ADU loan specialist (Maxable)

Compare Your ADU Financing Options (quick table)

| Option | Best for | How funds are delivered | Can keep low-rate 1st? | Typical constraints |

|---|---|---|---|---|

| HELOC | Flexible draws, phased work | Revolving line; draw as needed | Yes | Variable interest; subject to lender CLTV caps. |

| Home-equity loan (fixed 2nd) | Predictable monthly payment | Lump sum; fixed rate | Yes | CLTV-limited; rates often higher than first-lien mortgages. |

| Cash-out refi | One payment, large budget | Lump sum at closing | No (replaced) | Today’s market rate; closing costs apply. |

| Construction → permanent | Low equity / big build | Milestone draws; then converts | No (usually) | More docs/inspections; refi at conversion; underwrites on after-improvement value. |

| 203(k)/HomeStyle® | Purchase + ADU or refi + ADU | Funds based on after-improvement value | No (program refi/purchase) | Program rules, approved contractors, MI/fees. |

| SDHC ADU Loan | Moderate-income owner-occupants (City of SD) | Up to $250k; 1% construction → 4% fixed permanent | Varies (first or second lien) | 7-yr affordability covenant; 75% LTV; 680 FICO; income caps. |

How to Choose

- Decide whether to keep your first mortgage. If it’s a low rate, favor Home Equity lines of credit (HELOC) or a home-equity loan so you preserve it—“the advantage is you keep your low-rate primary mortgage.” — Will Johnson via NerdWallet

- Size your budget vs. equity. If lender CLTV limits won’t cover your scope, consider construction or renovation loans that underwrite on after-improvement (future) value and fund in draws—e.g., refi-plus-renovation paths outlined by NerdWallet.

- Leverage local incentives. If eligible, the San Diego Housing Commission (SDHC) ADU Finance Program can materially lower borrowing costs in exchange for a 7-year affordability covenant—useful whether your ADU is a conversion or detached unit. (SDHC)

Pro Tips

- “The main advantage to borrowing equity is that you keep your low-rate primary mortgage.” – Will Johnson (San Diego broker), noting “the advantage is you keep your low-rate primary mortgage.” (NerdWallet)

- “A lot of times people… think their ADU will cost 100 grand and it’s 300 grand. That’s going to stop the loan process in its tracks.” – James Carmody (Synergy One Lending), warning that underestimating costs can derail financing. (Maxable interview)

Start Your ADU Project with Better Place Design & Build

Get a free site assessment and financing roadmap – we’ll align scope, timelines, and a funding path you can qualify for, comparing Home Equity lines of credit vs. refinance vs. SDHC before you pay design fees. In one consult, we’ll compare equity and refi options (including construction financing that uses after-improvement value and HomeStyle® Renovation/FHA 203(k)), confirm eligibility for the SDHC program, and review fees and permitting basics to keep the budget realistic. To get started, call 858-355-9766 or visit our Contact Us page.

Pro tip: book the consult before paying design fees—align scope with the right financing path (HELOC vs refi vs SDHC) and confirm fees/permits to keep your ADU budget realistic.

FAQs About ADU Financing

There’s no single “best” loan product—the right choice depends on your equity, interest rate, and budget. If you have a low-rate first mortgage and solid equity, a HELOC (Home Equity line of credit) or fixed home-equity loan lets you keep that rate. If equity is tight or you need funds in stages, consider construction financing or a renovation mortgage such as Fannie Mae HomeStyle® or FHA 203(k) that underwrites to the home’s after-improvement appraised value. In the City of San Diego, eligible owner-occupants should also evaluate the SDHC ADU Finance Program for below-market terms.

Prefab can trim design/build time and sometimes modestly reduce costs, but total budget still hinges on site work, utilities, permits, and finishes. In San Diego, realistic all-in planning ranges apply to both prefab and stick-built, and garage conversions can be cheaper if the structure is sound. Compare apples-to-apples scopes (foundation, hookups, fees, interiors) before deciding.

The statewide CalHFA $40,000 ADU Grant is fully allocated and not accepting new applications. Homeowners should monitor for future funding rounds and, locally, check city or county programs such as San Diego’s SDHC ADU Finance Program.

An attached addition often costs less per square foot because it can share structure and utilities with the main home. An ADU typically runs higher per square foot since it’s a self-contained residence with its own kitchen and bath—and may require separate utility work—but it can generate rental income and benefit from California’s impact-fee waiver under 750 sq ft. The right choice comes down to your goal: more living space for your household (addition) versus a rentable, independent unit (ADU).

More Blogs

-

ADU Trends & Insights

What Is a Casita? Definition, Uses, and How It’s Different From an ADU

Casitas are stylish, small ADUs under 800 sq. ft., perfect for guests, rentals, or in-law suites. Discover the benefits, costs, and designs.

-

ADU Trends & Insights

What Are Stacked Accessory Dwelling Units (ADUs)?

Stacked ADUs are two fully independent accessory dwelling units built vertically in a single two-story structure, allowing California homeowners to add multiple homes on one lot without increasing the building footprint when local height and zoning rules allow.

-

ADU Trends & Insights

How to Build an ADU in the San Diego Coastal Zone

Building an ADU in San Diego’s Coastal Zone requires checking if the property is in the Coastal Overlay Zone, which typically triggers a Coastal Development Permit or exemption.

-

ADU Trends & Insights

What Is ADU Rental Income and Why Are California Homeowners Investing in It?

Explore how to maximize rental income from an ADU with tips on design, rental strategies, and legal considerations to turn your ADU into a profitable investment.

-

ADU Trends & Insights

Setback Requirements for ADUs in San Diego

Ensure your ADU meets California's setback requirements—learn essential rules, local variations, and expert tips to maximize your space and streamline permitting.

-

ADU Trends & Insights

Should You Build Your ADU Yourself or Hire a Contractor in San Diego, California?

Building your own ADU in San Diego can save on labor and contractor markup, but it’s essentially managing a small-house build with permits, trades, and inspections—so hiring an experienced contractor (or using a hybrid approach) often reduces delays, risk, and costly mistakes.

-

ADU Trends & Insights

Custom ADU: Your Ultimate Guide

A custom ADU may cost more than manufactured or prefab units, depending on size, type, and finishes, but it offers several benefits.

-

ADU Trends & Insights

13 Common Misconceptions About ADUs

Uncover the truth about ADU misconceptions and navigate construction, costs, and regulations for informed decisions.

-

ADU Trends & Insights

What Is an ADU Cost Breakdown?

An ADU cost breakdown shows where your budget goes—hard construction costs (about 85–90%) versus soft costs like plans, permits, and city fees (about 10–15%)—so you can set realistic expectations and avoid surprises.

-

ADU Trends & Insights

20 Day Preliminary Notice for ADUs in California: Requirements and Deadlines

A California 20-Day Preliminary Notice is a required filing for most ADU projects that subcontractors and suppliers must send within 20 days of providing labor or materials, notifying owners, contractors, and lenders.

-

ADU Trends & Insights

Are ADUs a good alternative to nursing homes for California homeowners?

ADUs offer California homeowners a practical alternative to nursing homes by allowing aging parents to live independently on the same property, supporting aging in place while turning ongoing care costs into a long-term home investment.

-

ADU Trends & Insights

What Are ADU Owner Occupancy Requirements?

ADU owner occupancy requirements are rules that require a property owner to live on the same lot as an accessory dwelling unit, either in the primary residence or the ADU itself. These rules were historically imposed by local governments to discourage absentee landlords and preserve neighborhood character. In California, however, owner-occupancy requirements for ADUs are […]

-

ADU Trends & Insights

What Are ADU Electrical Requirements in California?

Get the complete breakdown of electrical requirements for ADUs in California, from panel upgrades to solar compliance, to help you build safely and within code.

-

ADU Trends & Insights

Construction Loans vs. Personal Loans for ADUs: What Do California Homeowners Need to Know?

Building an ADU in California typically requires high financing and San Diego homeowners usually choose between construction loans, which are based on the future value of the property, and personal loans, which offer fast approval but higher interest rates.

-

ADU Trends & Insights

Should You Invest in Building an ADU in San Diego?

Building an ADU in San Diego can be a worthwhile investment for homeowners looking to generate rental income, increase property value, or create flexible living space for family members. An Accessory Dwelling Unit (ADU) is a secondary residential unit built on the same lot as a primary home, and demand for ADUs continues to grow […]

-

ADU Trends & Insights

Can an HOA Prevent an ADU in California?

If you’re part of a homeowners association and considering building an accessory dwelling unit on your property, it's key to consider any rules your HOA may have about ADUs.

-

ADU Trends & Insights

Prefab ADUs: Pros and Cons

Explore the pros and cons of prefab ADUs in California, including cost, customization, durability, and ROI, to decide if modular construction suits your needs.

-

ADU Trends & Insights

Do You Trust Your Builder?

You can trust your ADU builder when they prove real ADU experience, proper California licensing/insurance, and clear written contracts, not just a good sales pitch.

-

ADU Trends & Insights

What Are the Best Loan Programs for ADUs in California (San Diego Guide)?

California homeowners can finance ADUs through home equity, construction or renovation loans, cash-out refinancing, and programs like CalHFA (when available) and San Diego’s SDHC, with the best option depending on equity, income, and timing.

-

ADU Trends & Insights

SB9 vs ADU: What’s the Difference and Which Is Better?

While promising, the complexity and lengthy approval process of SB9 projects make traditional accessory dwelling units (ADUs) an often simpler and quicker alternative for expanding property use.

-

ADU Trends & Insights

How Does Choosing the Right Color Scheme Impact an ADU’s Design and Value?

Choosing the right ADU color scheme—especially light, neutral palettes with intentional accents—can make small spaces feel larger, improve livability, and increase rental and long-term property value.

-

ADU Trends & Insights

Where Can ADUs be Built in San Diego, CA?

ADUs are allowed on nearly all residential lots in California, including single-family and multifamily properties, under state law. In San Diego, any property zoned for residential use qualifies, making it easier than ever for homeowners to add an ADU and expand their living or rental space.

-

ADU Trends & Insights

How Do You Compare ADU Builder Quotes in San Diego and California?

Compare itemized ADU quotes—labor, materials, permits, timelines—to ensure transparent pricing, true value, and no surprise costs.

-

ADU Trends & Insights

How Do You Integrate Outdoor Living Into ADU Design?

Integrating outdoor living features such as patios, decks, and seamless indoor-outdoor connections helps ADUs feel larger, more livable, and more valuable.

-

ADU Trends & Insights

How Do You Budget for an ADU Build in California and San Diego?

Learn how to budget for an ADU in California and San Diego by understanding costs, timelines, financing options, and strategies to avoid surprises and maximize long-term value.

-

ADU Trends & Insights

Garage ADU: What It Is, Costs, Rules, and Conversion Options

Unlock your property's potential by converting your detached garage into a cost-effective, versatile ADU that increases property value and generates rental income.

-

ADU Trends & Insights

Why ADUs & Costs Matter in San Diego

Planning an ADU in San Diego? Get the lowdown on all the hidden costs that can catch you off guard.

-

ADU Trends & Insights

Can You Sell an ADU in San Diego?

San Diego's pending ordinance may soon enable homeowners to sell ADUs as separate condominiums, expanding affordable housing opportunities.

-

ADU Trends & Insights

What Roofing Options Are Best for ADUs in California (Especially San Diego)?

The best ADU roofing in California (especially San Diego) balances budget, durability, and curb appeal—using options like asphalt shingles, metal, tile, or low-slope membranes that meet Title 24 cool-roof/solar requirements and hold up to intense sun, heat, and wildfire risk.

-

ADU Trends & Insights

What is stormwater management for Accessory Dwelling Units (ADUs) in California?

Stormwater management for ADUs is the process of controlling and treating rainwater runoff generated by new backyard cottages or secondary homes.

-

ADU Trends & Insights

Downsizing to an ADU: Benefits, Costs, and Key Considerations

Downsizing to an ADU means moving into an Accessory Dwelling Unit—a smaller, self-contained home on your property—while renting out or repurposing your main house.

-

ADU Trends & Insights

California ADU Law: The Ultimate Guide

California has streamlined ADU construction to address the housing crisis, but development standards still apply. Check local regulations before starting your project.

-

ADU Trends & Insights

Why Do You Need an Experienced ADU Builder in California?

An experienced ADU builder helps homeowners navigate California’s complex permitting rules, zoning regulations, and construction requirements while avoiding costly mistakes and delays. Accessory Dwelling Units (ADUs) are secondary housing units built on the same property as a primary residence and can include detached backyard homes, attached additions, garage conversions, or basement apartments with independent living […]

-

ADU Trends & Insights

What Is a Retaining Wall for an ADU?

A retaining wall for an ADU is a structural wall designed to hold back soil, stabilize slopes, and create a level building area. These walls help prevent erosion, protect the structure from water damage, and make construction possible on sloped or uneven lots.

-

ADU Trends & Insights

What Are the Best Floor Plans for ADUs?

The best ADU floor plans are goal-driven and code-compliant—using efficient layouts like studios, 1-bed/1-bath rentals, or split-bedroom designs that maximize light, privacy, and flexibility while fitting your lot and budget.

-

ADU Trends & Insights

Are Pre-Approved ADU Plans Right for You in San Diego?

Compare pre-approved vs. custom plans and why the cheapest option isn't always best.

-

ADU Trends & Insights

What are the universal design principles for ADUs?

Universal design principles for ADUs focus on creating safe, flexible, and comfortable homes—using features like step-free entries, wider doorways, accessible bathrooms, and intuitive layouts—so the space remains usable for people of all ages and abilities over time.

-

ADU Trends & Insights

Is it Worth It To Build An ADU in 2026? Assessing the ROI of Building an ADU

Discover the financial benefits and pitfalls of building an ADU with our comprehensive, detailed guide.

-

ADU Trends & Insights

What Qualifies as an ADU?

ADUs are reshaping the California housing market, providing homeowners with cost-effective, independent living spaces to meet diverse needs.

-

ADU Trends & Insights

How Do You Design the Perfect Granny Flat?

Designing the perfect granny flat starts with understanding local ADU regulations, defining the unit’s intended use, and planning a layout that maximizes comfort within a compact footprint. In California, granny flats—legally classified as Accessory Dwelling Units (ADUs)—must comply with state and local rules covering size, setbacks, and permitting. A successful design balances budget, livability, and […]

-

ADU Trends & Insights

What Are Vaulted Ceilings and High Ceilings in ADUs and Are They Worth It in California?

Vaulted ceilings enhance ADUs by maximizing vertical space, increasing natural light, improving comfort, and boosting long-term property value in California when designed and built correctly.

-

ADU Trends & Insights

How Long Until an ADU Pays for Itself?

Most ADUs pay for themselves within 5–15 years by combining rental income and property value appreciation, with faster payback in high-demand markets like San Diego.

-

ADU Trends & Insights

What is the importance of an ADU feasibility study in California and San Diego?

An ADU feasibility study is a comprehensive analysis of zoning, site constraints, existing utilities, and a proposed design that determines whether building an accessory dwelling unit is practical and financially viable on a specific property.

-

ADU Trends & Insights

What Are the ADU Electrical Requirements in California in 2026?

California ADUs must comply with strict electrical and energy regulations under the California Electrical Code (CEC) and Title 24 energy standards. Most ADUs require detailed planning for electrical panels, load calculations, dedicated circuits, solar readiness, and utility coordination to meet modern safety and efficiency requirements. Homeowners in San Diego and across California often underestimate the […]

-

ADU Trends & Insights

How do ADUs benefit real estate agents in California and San Diego?

ADUs benefit real estate agents in California and San Diego by increasing property value and buyer appeal, creating built-in rental and multigenerational living opportunities, and giving ADU-savvy agents a competitive edge in pricing, marketing, and closing deals in a tight housing market.

-

ADU Trends & Insights

What Makes an Ideal Lot for an ADU in California (Especially San Diego)?

An ideal ADU lot in California (especially San Diego) is flat or gently sloped with enough clear buildable space for setbacks, good construction access, nearby utility tie-ins, and minimal easements or overlays—since slope, access, and utility distance are the biggest drivers of cost and feasibility even with “by-right” ADU rules.

-

ADU Trends & Insights

When Do You Need a Survey for an ADU in San Diego?

A survey for an ADU in San Diego is typically required when the new unit is built close to property lines, situated on a sloped or irregular lot, or when local regulations mandate setback verification.

-

ADU Trends & Insights

How Many ADUs Can You Have on Your Property in California?

Understand California's rules for ADUs and JADUs, including property limits, zoning laws, and strategies to maximize space, rental income, and property value.

-

ADU Trends & Insights

When Should You Build an ADU in San Diego?

ADU construction involves planning, permitting, and building a self-contained living space on a residential property — adding value, flexibility, and income potential without buying new land. In California, ADUs now make up about one in six new homes, reflecting their growing role in solving the state’s housing shortage.

-

ADU Trends & Insights

How Much Does an ADU Increase Property Value?

Discover how adding an ADU can significantly boost your property value, generate rental income, and enhance long-term equity—all while making the most of your available space.

-

ADU Trends & Insights

Using a HELOC to Fund an ADU in California?

A HELOC lets California homeowners fund an ADU in phases using home equity, paying interest only on what they use. In San Diego, strong rental income often offsets payments, though variable rates and post–draw-period repayment increases should be considered.

-

ADU Trends & Insights

The Perfect ADU Kitchen

Discover how smart layouts and stylish design choices can transform even the smallest ADU kitchens into luxurious, functional spaces.

-

ADU Trends & Insights

What Is a Granny Flat? Definition, Types, and How They’re Used

Granny flats offer San Diego homeowners flexible housing solutions, from accommodating family to generating rental income, with options including detached builds, garage conversions, or junior ADUs.

-

ADU Trends & Insights

Best ADU Designs

Explore essential ADU design trends and practical insights, from layout optimization to style choices, ensuring your accessory dwelling unit maximizes comfort, functionality, and investment potential.

-

ADU Trends & Insights

ADU vs JADU: What’s the Difference?

Explore the crucial differences between ADUs and JADUs—including size, regulations, costs, and ROI—to determine the best fit for your property and goals.

-

ADU Trends & Insights

ADU Manufactured Homes in San Diego: Are They Right for You?

Discover whether a manufactured home is the right choice by exploring costs, regulations, benefits, and potential drawbacks.

-

ADU Trends & Insights

How Does ADU Construction Work in San Diego, CA?

San Diego’s ADU process is fast and flexible, with permits approved within 60 days and options for detached units up to 1,200 sq. ft. or garage conversions. Thanks to state laws and the city’s ADU Bonus Program, homeowners can build quickly, add value, and even earn extra units by including affordable housing.

-

ADU Trends & Insights

What Is ADU Construction?

ADU construction involves planning, permitting, and building a self-contained living space on a residential property — adding value, flexibility, and income potential without buying new land.

-

ADU Trends & Insights

Spanish Style ADUs

Explore the timeless elegance of Spanish-style ADUs with iconic features like stucco walls, red tile roofs, and stunning architectural details.

-

ADU Trends & Insights

What Are the Legal Bedroom Requirements in California?

California has made building ADUs easier to tackle the housing crisis, but specific state and local regulations still apply. Here's what you need to know before starting.

-

ADU Trends & Insights

What Is an ADU Cost Calculator and How Much Does It Cost to Build an ADU in California?

An ADU cost calculator helps California homeowners estimate the cost of building an accessory dwelling unit based on factors like square footage, construction type, utility work, site conditions, and finish quality. In California, ADU construction costs typically range from $100,000 to $200,000, although detached ADUs with premium finishes or difficult site conditions can exceed that […]

-

ADU Trends & Insights

Key Differences Between Pool Houses and ADUs

Discover the differences between pool houses and ADUs to choose the right addition for your property—find out about amenities, regulations, and value impact!

-

ADU Trends & Insights

How We Make Your ADU’s Interior Design Stress Free & Feel Like Home

Our interior designers simplify the finish selection process—so you get a stylish, renter-friendly ADU without the stress, delays, or costly mistakes.

-

ADU Trends & Insights

How to Finance an ADU Project in California

California homeowners can finance an ADU using home equity, cash-out refinancing, construction or renovation loans, and programs like San Diego’s SDHC (up to $250K), with rental income often helping offset the $200K–$450K build cost.

-

ADU Trends & Insights

What Is ADU Project Management?

ADU project management is the process of overseeing every stage of an accessory dwelling unit project to ensure it stays on schedule, within budget, and compliant with local regulations. It involves coordinating architects, contractors, and inspectors while managing permits, timelines, and construction milestones. Effective project management also includes tracking costs, minimizing delays, and maintaining clear […]